China’s economy has overgrown over the last few decades, making it the second largest in the world. The flourishing real estate has always contributed to China’s economic progress. Over the previous decade, China’s real estate sector has persistently depended too heavily on high levels of property ownership, raising the ratio through a variety of tactics to achieve asset and company growth. China’s biggest real estate corporation has an asset-liability ratio that exceeds 80%. As a result, it has historically posed a real estate crisis in the country. However, one of the most important economic and social challenges facing the Chinese people is housing affordability due to the high cost of homes, which is disproportionate to their salaries and earnings.

When the People’s Republic of China was founded in 1949, it inherited the real estate system from the Soviet Union: the Welfare Housing System. In this system, the real estate sector isn’t privatized. Under this arrangement, all properties belong to the government’s agencies. China presented “the one-third model,” a new real estate model, in the second phase (1978–1987). Under this model, government-owned businesses, the government, and private citizens all pay for new homes’ building and upkeep costs.

During the third phase (1987-91), real estate in China gradually entered the market. Some cities and provinces were granted the permission to construct and conduct land transactions. “In addition, the housing Public Accumulation Fund (PAF), contributed to by employees and aimed to relieve the financial burdens of employers, was launched in Shanghai and gradually spread to other parts of China” (Fung-Hung Gay et al.: 73) This marked the ongoing enhancement of China’s housing infrastructure. Under the fourth Phase, from 1992 to 1997, China’s property industry expanded significantly. Following the establishment of economic development zones in many Chinese regions in 1992, land use regulations were relaxed and an enormous amount of relevant real estate service businesses—such as property management and brokerage firms—were founded. Phase five started in 1998 with a surge in property prices in China’s real estate sector. The Welfare housing system was to be eliminated by the government, and a “welfare” planned system transformed into a housing subsidy system. As per reports, by 1990s China completed the process of marketization of real estate, alongside the market reforms which Beijing had embraced in the 1980s. During this period, China’s real estate market entered the era of unprecedented prosperity. It was during this phase that Evergrande entered the Chinese real estate market.

Genesis of Evergrande:

Evergrande was a Chinese property developer company, having the second largest sales and was founded by Hui Ka Yan in 1996. The company is headquartered in Nanshan District, Shenzhen, China. Initially, China Evergrande Group was known as Hongda Group. With over 3,000 projects in China, a total governing area of over 509 million square meters and a total contracted area of over 812 million square meters, Evergrande Property Services Group, an industry tycoon of management enterprise in China, has been providing property services to approximately 3.3 million owners in China for more than 20 years. As per the company operates under the motto of “Conscientious services and heartfelt companionships”. In October 2009, as per the Wall Street Journal, the company conducted an initial public offering on the Stock Exchange of Hong Kong, raising USD 722 million.

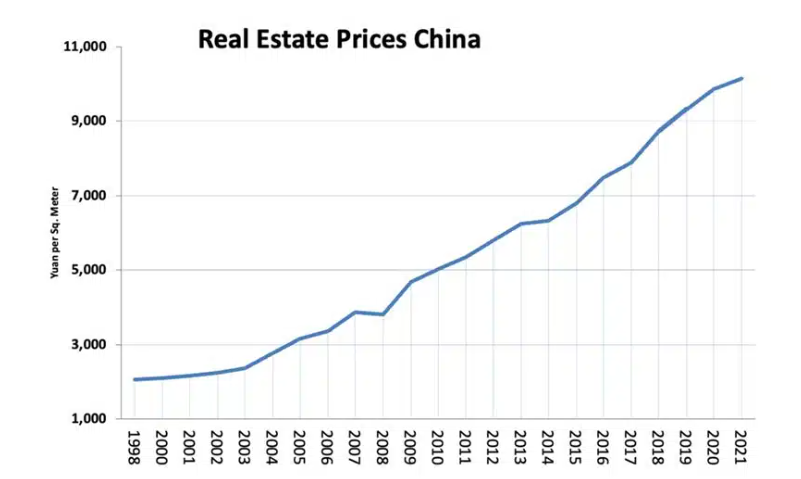

As China’s economy started to expand at one of the fastest rates in the world, rising levels of disposable income resulted in a boom in housing prices. As shown in the figure below, real estate prices rose at a steep rate, thereby resulting in an affordability crisis.

Figure 1: Rise in the prices of the Chinese Real Estate Sector from 1998-2021

Source: National Bureau of Statistics of China (2022/23)

After performing consistently for two decades, the developer group became the most valuable real estate company ($39.28 billion) in the world in 2018 stated by Xinhuanet News Channel. However, it was not immune from fluctuations in global real estate markets. As China embarked on its journey in the 21st century, it greatly enhanced its overall national strength. It emerged as the second-ranking powering the world by economic prowess.

As per an article written by CKGSB Knowledge, since 2005, the net profit margin of the real estate industry has only been 10%, the Return of Equity was 11% and the Return of Investment Capital was just 5.7%. The fact that the investment turnover ratio was only 45% explains the reason why net profits were as low as 10%. Developers bought up to 4.2 billion square meters of land from 2001 to 2011. In the same period the total area of completed housing was 6.5 billion square meters. Assuming that the average floor area ratio (land size to floor area) is 2.5 across 100 cities in China – by calculation the land which developers owned should have been 2.6 billion. This means they were hoarding 1.6 billion square meters of land. This was largely due to low financing options, as explained later in the article.

Moreover, the Ministry of Land and Resources published a set of regulations to prevent land hoarding between 2000 and 2008. The regulations stated that property companies would be charged a levy equal to 20 per cent of the land transfer fee if the land was left undeveloped for a year and that the state would be entitled to reclaim the land without paying compensation if it remained undeveloped for two years. Owing to unconducive policies and market pressures, Xi Jinping inherited a weak, faulty and imbalanced real estate sector in 2013.

Against this backdrop, the paper studies how the real estate sector performed during Xi’s era and what led to the ultimate demise of the Evergrande group.

Xi-Jinping Era: Xi Jinping has served as the secretary of the Chinese Communist Party (CCP) since 2012 and as the President of China since 2013. The decade under Xi’s leadership from 2012 to 2022, was a pivotal one. Since President Xi came to power, China’s economy has grown manifold. From 1980- 2021, China’s GDP has grown at an average rate of 10% and since Xi took power, the GDP has almost doubled, from $8.53 trillion to 17.73 trillion. He focused on the campaign to modernize the military in China, which mainly called for faster military growth. One of the key moves was the strict “zero-covid policy”, which had a bang on the unemployment rate, along with lockdown. According to NBC News on 22 October 2022, by Jennifer Jett, JoElla Carman and Alex Ford, During Xi’s time, US-China relations are widely considered to be at their lowest point since the two countries established diplomatic ties in 1979.

Population policy, demographics, and Rise of Ghost Cities: According to China’s National Bureau of Statistics in January 2024 the Chinese population displays an annual growth rate of -0.15% in 2023. As of 2023-24, China now stands second concerning population after India. China’s “One Child policy” was a major factor in the decline of the population. China’s dependent population is about 46% as of the seventh National Chinese Population Census 2022. Demographics of the country have caused an increase in ghost cities making them more prevalent across the country. The structural risk in China compromises long-term economic prospects. As effective housing demand was dropping, local governments continued to sell large amounts of residential and commercial land under the CCP’s entrepreneurial administration, resulting in an oversupply relative to real demand. The Chinese real estate boom resulted in higher property values, which in turn encouraged developers to construct additional infrastructure. However, the demand has recently dropped dramatically as a result of declining population growth and rapid ageing of the population, rising housing prices, low consumer confidence in the economy, and sluggish economic growth. Additionally, all of these resulted in rapid urbanization under an unsustainable model, creating inequality both within and between regions. China’s youth employment statistics paint a contradictory picture. The youth unemployment rate has reached double digits, but there is also a trend known as “tang ping”—a Chinese word for individuals who work intermittently so they can afford to pursue their interests. They avoid the corporate employment rat race, states Mr Balasubramanian C, a China watcher and Senior Research fellow with the Centre for National Security studies, Bengaluru. With a falling population and unfavourable demographics, the real estate sector has become an Achilles heel for the country. Chinese Economists and analysts grew fearful of Xi Jinping’s isolationist administrative policies because they believed that closing loopholes would negatively impact the economy. The lack of necessary data on any facet of the Chinese economy has prevented small and medium-sized enterprises from accessing the market.

Covid and Evergrande Crisis: At the onset of the pandemic in 2019, the average revenue of the Evergrande group increased, but so did the overall cost. Thus, their net profit has decreased, like most of the real estate companies at the time. Liabilities increased and the share prices, dividends and also the gross profit significantly reduced post mid-2021. The huge gap in cash flow also led to the major downfall of Evergrande during COVID-19. In 2021, Evergrande’s interim report showed 1.97 billion yuan of liabilities. On the morning of March 21, the Hong Kong Stock Exchange announced that China Evergrande, Evergrande Auto, and Evergrande Property were officially suspended from trading at 9:00 a.m. The company defaulted in 2021. It was around $300 billion in debt. This marked the ultimate closure of Evergrande.

Financing risk: From the year 2020, the symptoms were clear, the asset-to-debt ratio of China Evergrande Group is shown to vary around 85%. The Group had surpassed its asset-liability ratio danger line, which stands at 80%. Maintaining an asset-liability ratio between 60% and 70% makes more sense when looking at it from the standpoint of the real estate sector alone. Nonetheless, China Evergrande Group’s asset-liability ratio is far more than what is considered reasonable for the real estate sector. Thus, it was evident that the financial leverage coefficient of China Evergrande Group is high and that both its short and long-term solvency are fragile.

Cash flow risk: Evergrande Real Estate Group’s negative cash flow from investment activities in 2019 suggests that the business may have lost money on bad investments. Evergrande Group’s sales revenue is less than its costs, its operating activities have been using up cash steadily in recent years, putting its operations at risk. This is reflected in the negative net cash flow from operating activities.

However, the net cash flow of Evergrande Real Estate Group’s investment activities from 2017 to 2020 was negative, and the net cash flow of operating activities alternated between positive and negative, suggesting that Evergrande Group will spend the accumulated funds before. It was clear that there was a higher chance that the China Evergrande Group wouldn’t be able to pay back its debts when they were due.

Xi Jinping’s most notable work was the introduction of the three red-lines policy in August 2020. The policy shed light upon the real estate sector, comprising of the following ratios:

a) High Cash-to-short-term debt ratio – For more than a decade, the Chinese economy has been debt-driven, while creating an illusion of prosperity. In simple words, they have more debt or loans than disposable cash in hand. The larger the scale of the company, the easier it was for it to borrow, and faster for it to develop, despite high debt. Because of this debt-driven business model, the new rules made it difficult for firms to have a cash-to-short-term debt ratio of 1:1. In simple words, for 1 Chinese Yuan of cash held by a firm, a firm could take a loan/debt of 1 Chinese Yuan, not more than that. This was done to encourage firms to be more “profit-driven”, as now the companies could not borrow as they could before.

b) Net gearing ratio of less than 100% – Also known as the “debt-to-equity” ratio, which measures how much of the company’s operations are funded by debt compared to its equity. A Net gearing ratio ideally between 25-50% indicates a better shareholder relationship. It simply means to depend on shareholders’ equity for funding, rather than to borrow, reducing the debt burden. The lower the ratio, the better the company performs during a financial crisis, simply by playing safe.

c) Liability to asset ratio of less than 70% – Also known as solvency ratio which measures how the company’s assets are made up of liabilities. An ideal liability-to-asset ratio falls between 0.3-0.6. A higher ratio indicates that a larger share of the company’s funds is a liability or a burden that should be repaid and they do not own it. The policy with a low ratio ensures control of the overbuying of land because more land means more leverage. Buying land now needed more research, skills and judging which land needs more investment. This aimed at reducing the debt in the real estate market.

In 2019, the net gearing ratio was 1.4, which was out of limits and the liability to asset ratio was 75%, which was also out of limits. The average cash to short-term debt ratio was 1.3, which was in limit out of the three ratios. These measures were brought to monitor and reduce the amount of debt in the real estate sector. The debt in real estate could have been raised due to the following reasons. According to the data released by the Shanghai E-house Real Estate Research Institute, in 2020 the price-to-income ratio in China’s first-tier cities is 26.6 whereas the average is 13.4. Secondly, as more and more people move to urban areas, the rate of urbanization increases, making the demand higher than the supply in the property market, leading to a price hike. These high property prices have led to the crowding-out effect on consumption. The companies and consumers were left highly leveraged, leading to huge amounts of debt.

After the implementation of the three red lines policy, consumer activity cooled down as the crises in the real estate sector were exposed. This also came as a jolt for the Evergrande sector. This was also one of the reasons for the emergence of “ghost cities” (as discussed above), in which hundreds of new cities produced a surplus of housing which remained under-utilized (Marcinkoski, 2015). However, there were many factors which explain the failure of Evergrande.

Causes of financial risks for Evergrande:

Evergrande’s financing was becoming more challenging due to the modification in real estate financing management policies. The asset-liability ratio, net debt ratio, and cash-to-debt ratio of Evergrande Group did not follow industry standards. Policy laws stated that Evergrande Group was not permitted to take on further debt in the upcoming year. This not only restricted the amount of bank loans and bonds that the Evergrande Group issued, but it also raised financing costs, which caused Evergrande’s liquidity risk to rise more quickly.

- Intense Competition, Low Product Profit Margins and High Financing Costs:

The “no speculation in housing” policy, severe industry competition, and slower product sales efficiency have all contributed to Evergrande Group’s weaker profitability. Products were also not getting sold quickly enough, inventory grew, and the company’s profitability declined due to low-profit margins. Liquidity risk was raised as a result of the declining asset quality, which left operating expenses unable to be paid for normally.

- Unreasonable Diversification Strategy Consumes Resources and Increases Debt Ratio:

Due to the haphazard diversification of its varied development strategy, which necessitated long-term capital expenditure to sustain mergers and acquisitions, the Evergrande Group’s industries had poor correlations with one another. Due to the inability to capitalize on the synergistic effects of diversification, the Evergrande Group’s varied sectors were primarily in a state of loss, necessitating ongoing funding to support the company’s growth in the Evergrande real estate business. To acquire money for diversification, Evergrande Group had to use all its current resources, which raised its debt ratio and raised its risk of liquidity.

In 2021, the business failed, and its total debt was estimated to be $300 billion. In June 2022, the company was served with a notice of lawsuit in Hong Kong by one of their investors. The property developer business was granted seven extensions totalling eighteen months by the court in Hong Kong. Afterwards, China Evergrande Group was asked to liquidate by Judge Linda Chan, in December 2023.

Since its inception in 1998, Evergrande has been a promising real estate player in China’s real estate landscape. However faulty financial policies and an unconducive government approach were the final nail in the coffin.

Disclaimer: The views and opinions expressed by the authors do not necessarily reflect the views of the Government of India and Defence Research and Studies

Title Image Courtesy:https://www.cfr.org/

References:

- Evergrande Group – About Evergrande URL: https://www.evergrande.com/en/About/Introduction

- Yang Chenrui et al. (2023), “The Impact of Three Red Lines Policy Real Estate Industry”, ResearchGate, URL:

- YU Hong (2014), “China’s “Ghost Cities”, ResearchGate, URL: https://www.researchgate.net/publication/290500071_China’s_Ghost_Cities

- Gaulard Mylene (2014), “The real-estate bubble in China”, ResearchGate, URL: https://www.researchgate.net/publication/286504449_The_real-estate_bubble_in_China

- CKGSB knowledge, (July 2022), “Series: China’s Real Estate Problem”, CKGSB Knowledge, https://english.ckgsb.edu.cn/knowledge/professor_analysis/series-chinas-real-estate-problem-3-the-two-bubbles-in-chinas-property-market/

- CKGSB knowledge (July,2022), “China’s Real Estate problem- Land Finance and local government revenue structures” URL: https://english.ckgsb.edu.cn/knowledge/professor_analysis/series-chinas-real-estate-problem-4-land-finance-and-local-government-revenue-structures/

- CKGSB knowledge (July,2022), “China’s Real Estate problem- The three red lines” URL: https://english.ckgsb.edu.cn/knowledge/professor_analysis/serhttps://www.researchgate.net/publication/373896412_The_Impact_of_Three_Red_Lines_Policy_on_Chinas_Real_Estate_Industry#:~:text=The%20Three%20Red%20Lines%20policy%20are%20financial%20regulatory%20guidelines%20in,the%20future%20stock%20changes%20ofies-chinas-real-estate-problem-1-the-three-red-lines/

- CKGSB knowledge (July,2022), “China’s Real Estate problem- The role of real estate companies” URL: https://english.ckgsb.edu.cn/knowledge/professor_analysis/series-chinas-real-estate-problem-2-the-role-of-real-estate-companies/

- Hong Ying et al (2023), “The Impact of COVID-19 on Evergrande: A Case Analysis”, ResearchGate, https://www.researchgate.net/publication/369435224_The_Impact_of_COVID-19_on_Evergrade_A_Case_Analysis

- BBC News, (January 2024), “Evergrande: Crisis-hit Chinese Property giant ordered to liquidate”, https://www.bbc.com/news/business-67562522

- Bloomberg News, (August, 2023), “China’s Debt-Fueled Housing Market Is Having a Meltdown, again”, https://www.bloomberg.com/news/articles/2023-08-23/china-real-estate-market-crisis-is-another-mess-for-xi-jinping?utm_source=website&utm_medium=share&utm_campaign=copy&leadSource=uverify%20wall

- Wang Lingyi (2022), “Analysis of the Causes of China’s Real Estate Bubble”, SHS Web of Conferences 154, 02010 (2023), https://www.shs-conferences.org/articles/shsconf/pdf/2023/03/shsconf_pesd2023_02010.pdf

- Miet Hannah (November 2023), “Will Xi Jinping’s Policies Continue to Hold Back China’s Property Sector-and Economy?”, Urban Land, https://urbanland.uli.org/economy-markets-trends/will-xi-jinpings-policies-continue-to-hold-back-chinas-property-sector-and-economy

- Fung Hung et al (January 2010), “Development of China’s Real Estate Market”, ResearchGate, https://www.researchgate.net/publication/46509750_Development_of_China’s_Real_Estate_Market

- Hu Ruolan (December 2023), “Motivation and Performance Analysis of SUNACs Deleveraging under the Three Red Lines Policy”, ResearchGate, https://www.researchgate.net/publication/376131491_Motivation_and_Performance_Analysis_of_SUNACs_Deleveraging_under_the_Three_Red_Lines_Policy

- Mingye Li (2017), “Evolution of Chinese Ghost Cities”, Open Edition Journals, https://journals.openedition.org/chinaperspectives/7209

- Low Justin (August 2023), “Houses are for living in, not for speculation-China state media”, forex live, https://www.forexlive.com/news/houses-are-for-living-in-not-for-speculation-china-state-media-20230823/

- Li Yini (December 2022), “The Impact of COVID-19 on China’s Real Estate Industry and the Outlook for Industry Trends”, ResearchGate, https://www.researchgate.net/publication/366296247_The_Impact_of_COVID-19_on_China’s_Real_Estate_Industry_and_the_Outlook_for_Industry_Trends

- Zhang, Gouyang (October 2022), “The History of China’s Real Estate Market and the risks it faces” URL: (PDF) The History of China’s Real Estate Market and The Risks It Faces (researchgate.net)

- Fung, Jeng (January 2010), “Development of China’s Real estate market”, (PDF) Development of China’s Real Estate Market (researchgate.net)

- South China Morning Post, (October 2021), What China’s Evergrande crisis means for the real estate market and the world, What China’s Evergrande crisis means for its real estate market and the world | South China Morning Post (scmp.com)

- Liu, yang (October 2020) “Productivity evaluation of the real estate industry in China: A two–stage Malmquist productivity index”, https://www.researchgate.net/publication/344485240_Productivity_evaluation_of_the_real_estate_industry_in_China_A_two-stage_Malmquist_productivity_index

- Wang, Shao, Wang; Yiti, Lei, Ya Ping (October 2018), “Pre-reform Welfare Housing estates in China: Physical Conditions and Social Profiles” Pre-reform Socialist Welfare Housing Estates in China: Physical Conditions and Social Profiles (tandfonline.com)

- Beijing Times, (October 2023), “China Evergrande Crisis: From “Too big to Fail to “Too Complex to Exist”? China Evergrande Crisis: From “Too Big to Fail” to “Too Complex to Exist”? – Beijing Times

- Sun, Li (April 2020), “Housing affordability in Chinese Cities”, Housing Affordability in Chinese Cities (lincolninst.edu)

- Series: China’s Real Estate Problem 1. The “Three Red Lines” – CKGSB Knowledge

- Reuters, (January 2024), “Timeline: Worsening crisis at Evergrande” https://www.reuters.com/business/worsening-crisis-evergrande-worlds-most-indebted-developer-2024-01-29/

- Wang, Ye, Zhu; Zexuan, Kesu, Dianying; (Advances in Economics, Business and Management Research, volume 219, “Financial analysis of Evergrande from the perspective of game theory” https://www.atlantis-press.com/article/125975360.pdf

- Zhao, Boya (2023), “Analysis on Financial Risk Management of China Evergrande group” article_1686232412.pdf (clausiuspress.com)

- Reuters, (January 2024), “China Evergrande unit starts legal proceedings against parent” China Evergrande unit starts legal proceedings against parent | Reuters

- Evergrande interim report 2023, intrep.pdf (irasia.com)

- Hong, Ma, Zing; Ying, Ziting, Huiying; (Vol.38,2023) “The impact of Covid-19 on Evergrande: A case analysis” (PDF) The Impact of COVID-19 on Evergrande: A Case Analysis (researchgate.net)

- Reuters, (January 2024), “China’s population drops for second with record low birth rate” China’s population drops for second year, with record low birth rate | Reuters

- South China Morning Post, (January 2024), “High Court orders Evergrande to wind up in Hong Kong’s biggest liquidation, as the world’s most indebted property developer reaches a dead end” High Court orders Evergrande to wind up in Hong Kong’s biggest liquidation, as the world’s most indebted property developer reaches a dead end | South China Morning Post (scmp.com)

- Xinhuanet, (May 2018), URL: China’s Evergrande tops world’s most valuable real estate brand: report – Xinhua | English.news.cn (xinhuanet.com)

- Wall Street Journal, (January 2014), URL: China’s Property Market Fueled Growth in 2013 – WSJ

- Jennifer Jett, JoElla Carman, Alex Ford; NBC News, 22 October 2022, “How China has changed under Xi Jinping, as shown in 9 charts” https://www.nbcnews.com/news/world/china-xi-jinping-third-term-rcna53346