The India-UK trade deal is an important milestone, which was signed on 24 July 2025 (Reuters, July 2025). It could add another £25.5 billion to bilateral trade by 2040. The deal matters, but the bigger question now is whether Britain wants to stop at the tariff agreement or wants a much deeper position in India’s industrial rise. A lot more business opportunities exist between the UK & India.

And that is where the comparison with other countries becomes important. France is already moving with India into Rafale jet and helicopter co-production, while Safran has said it is ready to open an engine assembly line in India (Reuters, February 2026). The United States already has the GE-HAL F414 engine co-production on track (Reuters, June 2023). Germany has moved into a submarine partnership with India (Reuters, January 2025). Australia has used its ECTA to strengthen its position in India’s critical minerals and resources sectors (DFAT Australia, ECTA outcomes), and Japan has built a semiconductor supply chain and economic security track with India (PIB, October 2023; PIB, August 2025) and concluded a warship production partnership. When others are moving faster, supporting India’s strategic growth cycle, Britain should not be lagging.

The 2030 Roadmap under Boris Johnson spoke about deeper cooperation in trade, investment, science & technology, defence, climate, and the Indo-Pacific (India-UK Roadmap 2030, May 2021). And then the UK launched the India FTA process in January 2022 (UK government, January 2022), and later, under Prime Minister Rishi Sunak. There were explicit steps on capital markets cooperation (UK government, September 2023). The earlier framework was not narrow at all; it was already pointing toward a much wider partnership, and perhaps that is exactly why it is reasonable to say that a larger industrial partnership is still possible, and it is half-open.

The present FTA covers sectors such as textiles, leather, marine products, gems and jewellery, chemicals, engineering goods, electronics and auto components. While also widening services in IT, finance, education, healthcare, professional services, telecoms and aviation support (PIB, July 2025). But India’s own CETA synopsis also makes clear that sensitive procurement-heavy ministries such as Defence, Home Affairs, Electronics and IT, and Space remain outside the deal (India-UK CETA synopsis, August 2025). Britain needs to go further into sectors where strategic trust, industrial policy and long-term capital all matter at the same time.

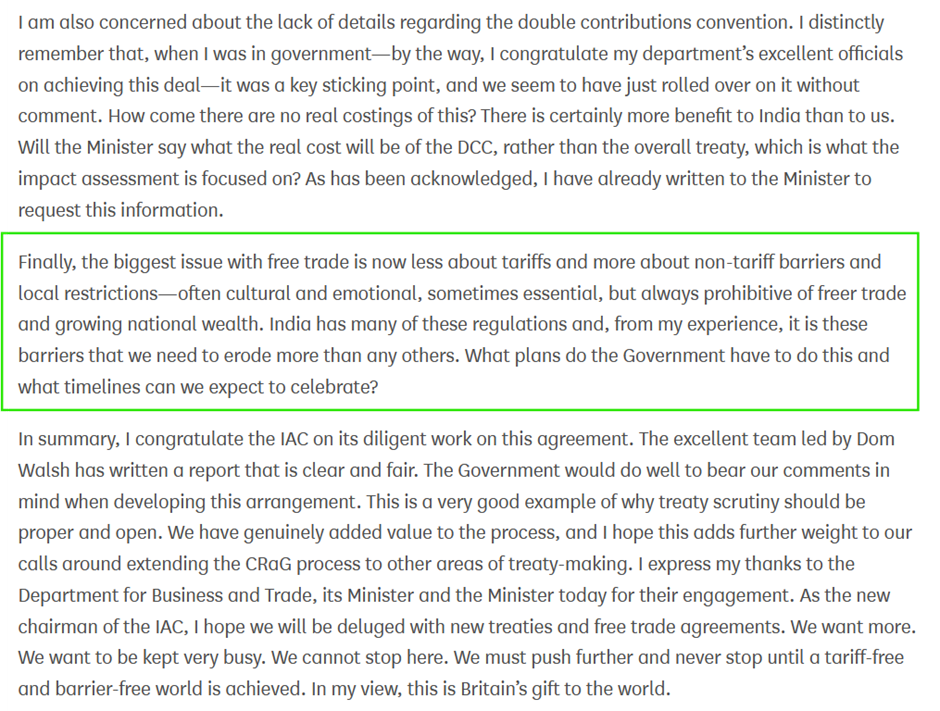

As Lord Dominic Johnson argued in the Lords, the real obstacle in trade now is often not tariffs but “non-tariff barriers and local restrictions” (Hansard, House of Lords, March 2026), and that is exactly why the next phase has to go beyond the signed text. The text of his speech in the house is placed below:-

The first among the sectors where India and the UK can collaborate is defence and aerospace. If France can move with Dassault and Safran, and the United States can move with GE and HAL, then Britain should be moving much more seriously with Rolls-Royce, MBDA and Babcock on one side targeting HAL, Bharat Dynamics, L&T and the wider AMCA. Reuters reported that India may need around 1,100 fighter-jet engines by 2035 and that Rolls-Royce was among the potential partners for that engine effort (Reuters, October 2025). The UK already has a live missile relationship with India; a tie-up with Bharat Dynamics, an Indian missile manufacturer, could reap benefits for the UK (Reuters, October 2025; Reuters company coverage).

The year 2030 vision document states that both India and the UK are committed to a partnership that delivers for both countries. The Vision is for revitalised and dynamic connections between the people, reenergising trade, investment and technological collaboration that improves life and livelihoods of citizens. Also to enhance defence and security cooperation that brings a more secure Indian Ocean Region and Indo-Pacific.

The second sector UK can pitch in is the maritime and the associated Indian Ocean security, including commerce. The old UK roadmap already highlighted the opportunities across the Indian Ocean and Indo-Pacific (India-UK Roadmap 2030, 2021). There can be a partnership between Babcock on the UK side and PSU shipyards on the Indian side. And these partnerships are possible not only in naval platforms but also in propulsion, maintenance, ship repair, port technology, undersea cable protection, marine electronics and logistics software. Babcock can lead a maritime partnership abroad effectively, similar to what it did in Indonesia. Mazagon Dock and Cochin Shipyard would fit into this endeavour.

The third sector is critical minerals, battery materials and downstream processing. Countries like Australia have already used ECTA to strengthen their position in India’s critical minerals and resources sectors (DFAT Australia). India itself is now putting more weight on critical minerals recycling and battery supply chains (Reuters, April 2025; Reuters, March 2025). Rio Tinto or Johnson Matthey of the UK could go along with Vedanta, Hindalco, Amara Raja and Tata Chemicals. These combinations can lead to better partnerships in processing, battery inputs, recycling and advanced materials.

The fourth sector is telecoms, cyber and semiconductors. Japan’s partnership with India shows that semiconductor and supply-chain cooperation can be built as part of a wider economic security framework (PIB, 2023 and 2025). While in the UK-India case, there is already a very tangible bridge in place through Bharti’s 24.5% stake in BT. Which the British government approved this stake after a national security review (Reuters, August and December 2024). BT-Bharti collaboration can take precedence over other trusted telecoms, digital infrastructure, and cyber companies across both nations.

The fifth sector is clean energy, hydrogen and Grid Transition. Boris Johnson in 2022 mentioned a possible offshore wind and a UK-India Hydrogen Science and Innovation Hub (Boris Johnson, April 2022). The UAE’s CEPA shows how a trade deal can quickly become a platform for much wider non-oil economic expansion (PIB, February 2025). Britain should now think practically and explore the extension of the tie-up between BP and Reliance (Reuters, 2019 and 2021) and a new partnership with Tata Power or even NTPC on the Indian side.

The sixth sector is financial services. Britain has a natural advantage by virtue of her experiance on financial and capital markets (UK government, September 2023). She could extend her services across finance, insurance, listings, risk cover, pension capital and even legal architecture. Which means HSBC and Standard Chartered can play a larger role from the UK side, against various indian entities. They would naturally fuel both countries’ industrial base since factories require capital and shipping/transportation requires insurance, and both can come from banks.

Life sciences and pharma can also be the sector where AstraZeneca and GS could collaborate with India’s pharma giants like Dr Reddy’s, Sun Pharma and Biocon. They could move forward with joint manufacturing, research, biologics, generics and supply resilience.

The FTA was good, useful, and necessary, but it should now be treated as phase one. Phase two should be a UK-India Trusted Strategic Sectors Corridor with two baskets, one for normal volume trade and the other for strategic sectors. Since both countries already have goodwill, and speak a common language in business and have a good FTA foundation, it could be used as a springboard for the next phase of strategic and business partnership.

References

Boris Johnson and Narendra Modi (2021) 2030 Roadmap for India-UK future relations. GOV.UK, 4 May.

Department for International Trade (2022) UK launches India negotiations to kick off 5-star year of trade. GOV.UK, 12 January.

Department of Foreign Affairs and Trade, Australia (2022) Benefits for the Australian critical minerals and resources sectors. Canberra: DFAT.

Hansard (2026) UK-India: Comprehensive Economic and Trade Agreement. House of Lords, 4 March.

Ministry of Commerce and Industry, Government of India (2025) India-UK-CETA: Synopsis of Key Chapters. New Delhi: Government of India, 6 August.

Press Information Bureau, Government of India (2023) Cabinet approves Memorandum of Cooperation between India and Japan on Japan-India Semiconductor Supply Chain Partnership. 25 October.

Press Information Bureau, Government of India (2025a) India-UK CETA: 99% Tariff Elimination, Stronger Bilateral Trade, Catalyst for Inclusive Growth. 27 July.

Press Information Bureau, Government of India (2025b) Fact Sheet: India-Japan Economic Security Cooperation. 29 August.

Press Information Bureau, Government of India (2025c) India-UAE Comprehensive Economic Partnership Agreement (CEPA) completes three years. 18 February.

Reuters (2019) BP to enter India’s fuel retail market with Reliance tie-up. 6 August.

Reuters (2021) BP-Reliance JV starts selling multiple fuels in India. 26 October.

Reuters (2023) GE to jointly produce fighter jet engines in India. 22 June.

Reuters (2024a) India’s Bharti to buy 24.5% stake in BT from Altice. 12 August.

Reuters (2024b) UK approves Indian group Bharti’s purchase of 24.5% stake in BT. 16 December.

Reuters (2025a) German-Indian JV emerges as sole contender for $5 billion India submarine deal. 23 January.

Reuters (2025b) India to formalise incentives for critical minerals recycling this year, sources say. 8 April.

Reuters (2025c) Britain and India sign free trade pact during Modi visit. 24 July.

Reuters (2025d) India expects $7.4 billion spending on fighter jet engines over next decade. 17 October.

Reuters (2025e) UK, Indonesia reach $5.24 billion maritime deal. 21 November.

Reuters (2026) India to make Rafale jets with France in boost to defence ties, Macron says. 19 February.

Reuters (n.d.) Bharat Dynamics Ltd. Company profile.

Reuters (n.d.) Cochin Shipyard Ltd. Company profile.

Reuters (n.d.) Mazagon Dock Shipbuilders Ltd. Company profile.

The Rt Hon Boris Johnson (2022) PM statement at press conference with Prime Minister Modi. GOV.UK, 22 April.

The UK Government (2023) Big steps forward in capital markets cooperation with India. GOV.UK, 11 September.

Title Image Courtesy: Deccan Herald

Disclaimer: The views and opinions expressed by the author do not necessarily reflect the views of the Government of India and the Defence Research and Studies.